Everybody is still hanging onto a process that 87 percent of Americans dislike.

Georg Bauer has worked in automotive finance for companies such as Tesla, BMW, and Mercedes-Benz; he’s currently the Co-Founder and President of Fair, an automotive finance company. Bauer believes that the autonomous car will disrupt the entire paradigm of car ownership and financing. Automakers are not only unprepared for the change, he says, they’re not even trying.

“We’re due for a makeover of the car buying and ownership process,” Bauer says. “The auto industry is 125 years old, and the industry has been charging ahead on the technology side. But if you look at the auto business today, the traditional buying process has experienced only marginal changes over the last 20 years. Everybody is still hanging onto a process that 87 percent of Americans dislike.”

A customer-centric paradigm

Bauer believes that the automotive industry is overdue for a fundamental change in the way we buy our cars, and the ways we pay for all the parts and services that keep them going.

“We’ve observed some consequences on the customer side, such as the push into leasing in the 1980s and 1990s. A lot has happened, and we’re now starting to realize that the industry is facing a revolution,” Bauer says. “What we’ve seen over the last 20 to 40 years was driven by technological changes and customer desires for a low monthly payment, or affordability, and things like that. But now it’s a revolution that will come in evolutionary stages.”

The good news for consumers is that new cars are likely to be much easier to manage.

We’ll no longer see individuals being insured, but cars and automakers will be insured.

“It still takes three hours or more to get all the paperwork in place when you buy a car, with all the insurance and DMV work,” Bauer tells Digital Trends. “It’s highly preventive and non-customer-centric. This customer-unfriendly process is going to change fundamentally.”

The key question, though, is what’s the new system going to be like?

“We have to completely reimagine the car-buying and ownership process,” Bauer insists. “For example, we could put together in one single monthly payment all the components of maintenance, insurance, parking, registration, fuel, and accessories. Today you have to schedule everything yourself, you have to pay separate bills and providers. It’s a completely antiquated process.”

But who’s going to change things? Not the people who make money off the current system, he notes.

“There’s a lot of thinking going on, and it’s hard to predict who’s going to be able to capture the new ownership experience. The OEMs and the dealers have to start to rethink this completely, but at the same time, I’m concerned whether they have the speed and agility to really move this forward. It’s possible that external players will step in to make it a less cumbersome process.”

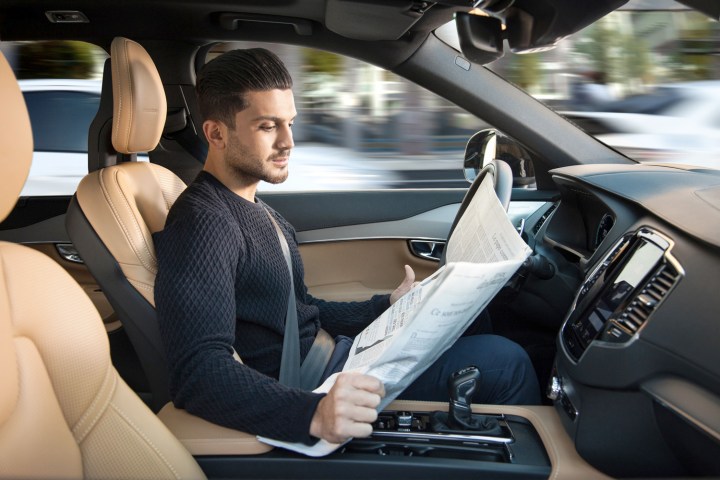

Enter the autonomous car

The inflection point that catalyzes fundamental change is likely to be the advent of the truly autonomous car in the next three to five years. Taken together with changes already happening in ride-sharing and mobility, autonomous cars are likely to accelerate changes in the traditional automotive economy.

“Paradigm shifts are never easy on those who dominate the markets, and that’s the automakers right now,” Bauer maintains. “With fully autonomous vehicles, over time the insurance situation will change completely. We’ll no longer see individuals being insured, but cars and automakers.”

Autonomous vehicles are also likely to spur the creation of new ownership models, with wide-ranging consequences.

“There will be more traditional people who want to keep owning the car as they used to, and others who will be addressing new concepts like mobility-as-a-service,” Bauer says. “Mobility-as-a-service could mean a monthly payment or individual ride-sharing. I think we’ll see subscription-based models of ownership where you change and get out of one car and get into a new one at certain times, providing flexibility.”

Potential for disaster

As electric vehicles come to us in concert with autonomous technology, the paradigm shift becomes massive. The biggest disruptions happen when large numbers of people seriously question the need to own a car at all. At that point, we could see a collapse of the entire automotive economy, which is currently structured around designing and building a car, selling it to you, insuring you, charging you for parking and maintenance, producing fuel and selling it to you, and providing you customized accessories.

In terms of jobs, the impact will be staggering. Automakers will still produce cars, but the traditional car dealership will fail. The local car repair shop will go away too, not to mention the car stereo place, the tire dealer, and the independent collision repair business. Look further ahead, and the corner gas station and the oil company behind it go away, as gasoline trends out of use in favor of electricity. With an autonomous car, the insurance industry doesn’t get to clip you for several hundred dollars a month, and even the local cop won’t be handing out tickets for speeding any more.

Even with all that economic disruption, this scenario could be optimistic. That’s because any artificial intelligence that is smart enough to drive a car may also be smart enough to take over your job, or mine.

The end of traditional auto finance

There’s one more implication of autonomous cars and new mobility. The traditional auto finance portfolio is going to go away — and that’s a huge amount of money.

“Right now there’s $1.1 trillion in auto finance loans, and another $400 billion in the ecosystem when you add maintenance and extended warranty and insurance,” Bauer says. “It’s a huge pie. The banks and the captive auto finance companies are going to have to get their act together or see this huge pie eaten by creative players.”

Captive auto finance companies are those like GMAC and Ford Credit, which are owned by the automakers, and exist to loan you the money to buy a GM or Ford vehicle. Honda, Toyota, Nissan, and all the other automakers have captive finance organizations, too.

Any artificial intelligence that is smart enough to drive a car may also be smart enough to take over your job, or mine.

“I don’t see the captive finance companies and the traditional auto lenders moving much in the direction that opens them up to a new and different way,” Bauer says. “Their contribution to a manufacturer’s overall earnings is 20 to 25 percent, and that’s a lot.”

If you’ve purchased a car recently, you were probably offered several attractive financing options by the dealer, with some funded by a local bank or credit union. What they didn’t explain to you is that the financial institution pays the dealer a substantial fee if you accept that loan. That doesn’t make it a bad deal for you, but it’s a major source of income on top of the price of the car for the dealer.

“I am here to make the prediction that this is all going to go away,” Bauer says. “As so often happens when the paradigm changes, the ones who own the business right now, they just think the cake will be around, but it’s going to go away and be replaced by different mobility ownership models. Autonomous driving triggers the change.”

When does this all happen?

Bauer believes the change will come faster than most people expect today.

“The investment the car companies are making is enormous,” he tells Digital Trends. “The companies that come out with autonomous first are going to have a competitive edge. We’ll be there in the next three to five years, but we also have to deal with the regulatory bodies. The lead will be in commercial fleets, but in five years plus, the consumers will take it on, provided the regulators are not lagging behind.”

“There’s a tipping point where you see acceleration. It’s not a question of whether it will come. It is going to come.”