Amidst the continued fervor for cryptocurrencies and blockchain technology, evangelists have claimed it can help replace everything from money itself, to the foundation of many of our digital tools. But with Bitcoin fees skyrocketing off of its expanded use last year, and bugged Ethereum smart contracts leading to users losing millions of dollars, is this really a technology that’s ready for mainstream adoption?

There’s not even a concrete definition of what a blockchain is. If, however, we assume it to be a distributed ledger system, there are key areas which many of those at the forefront of blockchain’s development believe are lacking. We sat down with blockchain developers to find out more about the technology’s flaws.

Working for everyone

This article is part of our series “Blockchain beyond Bitcoin“. Bitcoin is the beginning, but it’s far from the end. To help you wrap your head around why, we’re taking a deep dive into the world of blockchain. In this series, we’ll go beyond cryptocurrency and hone in on blockchain applications that could reshape medical records, voting machines, video games, and more.

“The biggest issue I see right now is the scalability problem,” Justas Pikelis, co-founder of blockchain Ecommerce platform, Monetha, told Digital Trends. “Right now, Ethereum can process 17 transactions per second. Facebook can handle 175,000 requests per second. Visa, 44,000 transactions per second. So, if we really want to use cryptocurrencies as currencies, it would not be possible as of this moment.”

The best example of blockchain’s scaling problem is the escalation of Bitcoin transaction fees and confirmation times that occurred during the currency’s explosive value rise at the end of last year. Fees rose from a dollar or two to as much as $50.

Other cryptocurrencies and blockchain platforms don’t suffer as severely from this issue, and there are technologies being implemented in Bitcoin to mitigate it, but it’s not an easy fix even with them in place.

“When you store the data on the blockchain, it’s quite expensive,” explained Alexander Demidko, CRO of blockchain database company Fluence. “That’s why all of those solutions are trying to store the data off chain and send it periodically to the blockchain. But it’s still hard to search through the data stored there. That’s why we [think] ideally there should be a way to upload the data to the decentralized environment, then search the data I need there. That’s what we’re trying to solve with a decentralized database, as it’s not currently supported by the blockchain.”

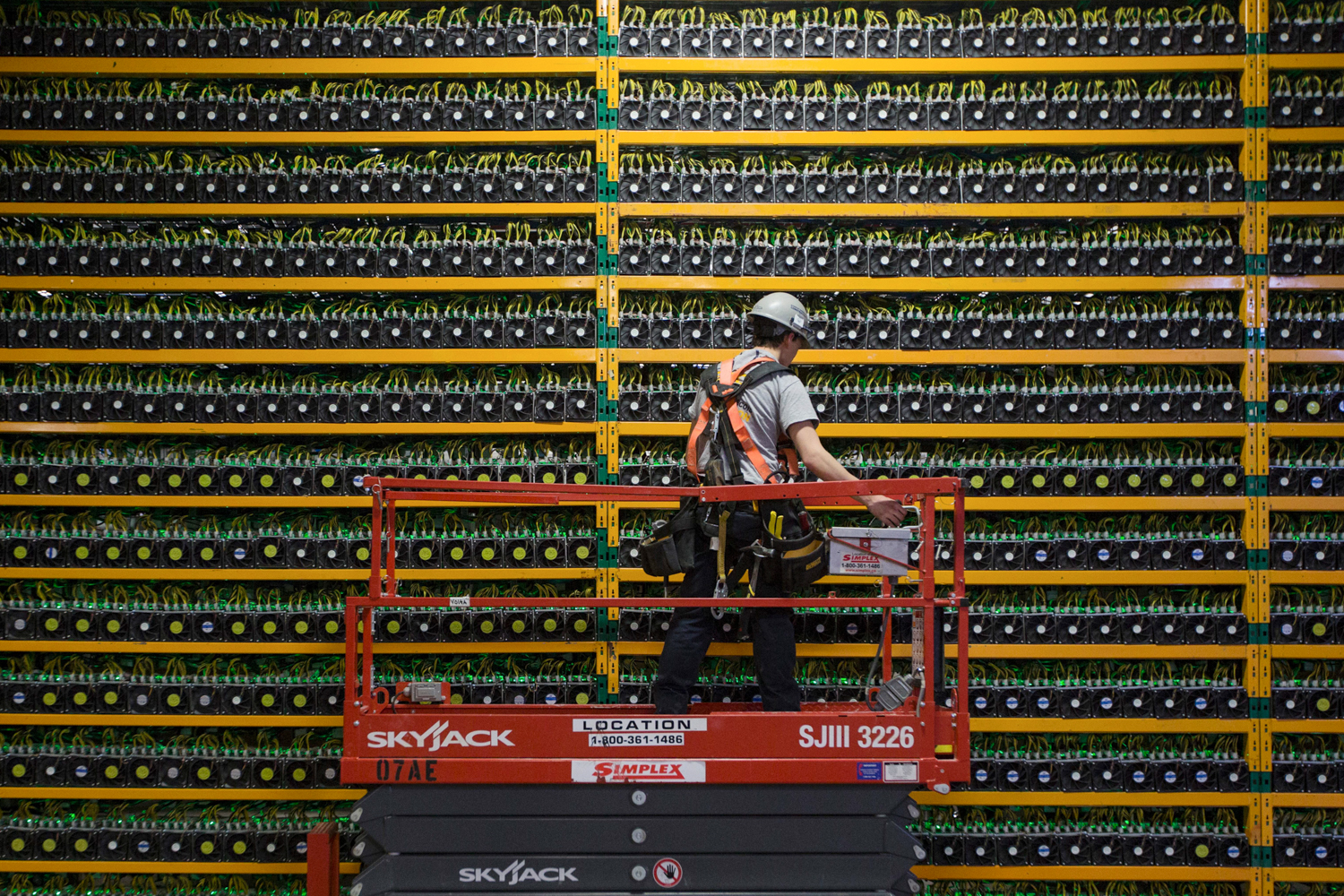

Blockchains like the one used by Bitcoin, which leverage a ‘proof of work’ system, require enormous amounts of computing power – that’s expensive in hardware and electricity. Although alternatives exist, blockchains are still computationally intense when compared with traditional databasing solutions. Storage is also a potential problem.

Bitcoin’s blockchain of simple transactions is upwards of 150GB. Any business institution using blockchain technology for a traditional database can expect every node to require much more space than that. That problem would be compounded if, as a company, you were to operate a private blockchain – controlling every node yourself.

Edgar Bers, head of public relations at HashCoins, believes blockchain technology, as it exists now, wouldn’t be useful or scalable for a large database.

“Most blockchains we have today are not good for businesses that rely on massive amounts of data […] Most businesses rely on terabytes of information and centralized server architecture […] Multi-terabyte blockchains are inefficient,” he said. “When your business requires ultra-heavy communications you really have to throw all the tech you can on the blockchain to survive the load. If you design a blockchain for a certain maximum of transactions per second, increasing your business operations could be staggering due to required blockchain upgrades – which you may not even have to hand.”

That’s less of a problem if you operate a public ledger blockchain because you can decentralize your blockchain over nodes that are found across the world. That’s certainly a viable solution, and one used by governments like Estonia. Yet that runs into another issue entirely. The problem of privacy.

For your eyes only

Most people imagine blockchain technology as the publicly distributed system that Bitcoin is built on. The nodes (miners) are located all over the world, and the entire blockchain is publicly downloadable, viewable, and verifiable. That total transparency creates all sorts of problems for organizations handling even the slightest confidential data.

“Full decentralization is almost utopian, where it can only be used in a very primitive function, like Bitcoin,” Pikelis explained. “When you’re talking about more complicated things, a little more information stored on the blockchain, it’s really hard to reach that full decentralization. Still people have to believe that companies are running these decentralized applications for them to be able to on board and really store the things and hash the things that are private [like] public information.”

Even the developers at Fluence, who are working on developing blockchain database technology that could, in theory, handle potentially sensitive information, don’t believe it’s quite ready to yet. “As with every technology that has yet to mature, you don’t want to store overly sensitive data there. Once it becomes more mature, you can trust it more,” Demidko told Digital Trends.

That’s not to say they aren’t working on a solution. The first and most predictable, considering the blockchain’s reliance on cryptography, is encryption.

“In the example of a driving license database, I am a user, I have my driver license and I want to put it into a decentralized database,” Demidko explained. “I can encrypt it with my personal key and not tell this key to anyone, but authorities who need that. If I put my driver’s license into the decentralized database, it’s encrypted there, so no other person can read it without my permission. The nodes where the data is being stored have access to the data, but they can’t read it because they don’t have any keys.”

However, encryption alone is not the final solution to privacy concerns. Private keys could be accidentally revealed by a third-party, and the development of quantum computing could lead to easy brute forcing of private keys that would threaten the sanctity of data stored on a truly decentralized blockchain. There’s no easy fix to these problems yet, so privacy will remain a serious obstacle for many promising projects.

The layman problem

Although blockchain technology is becoming easier to leverage and understand all the time, it’s still not an easy topic to get your head around. Blockchain services and tools demand more technical know-how from the users than many contemporary digital platforms, and that could prove problematic for adoption, especially if security scares and lost funds become associated with blockchain’s public image.

“Blockchain and Bitcoin [is] really hard for those who are not related to technology or software developers to use,” Fluence’s CEO, Evgeny Ponomarev told Digital Trends. “Just sending a transaction is pretty hard. The next year we all as a community need to build tools to make it easier, because it’s the only way to better adoption.”

Such tools will have to involve easier user security. Although blockchain technology is often more secure than traditional passwords, losing a private key can create all sorts of headaches. A decentralized system often lacks an arbitration process for recovery.

While blockchain is often more secure than regular passwords, losing a private key can create all sorts of headaches.

“There is some cryptography research that has been done with key recovery,” Ponomorev suggested, as a potential solution to this issue. “Splitting the key into many pieces, giving them to many people. They can help you recover it from pieces if you lose it. Some companies are trying to use a custodian system, where you can get your keys and place them somewhere or with someone safe, to protect you from losing keys.”

His company’s CRO quickly pointed out, however, that these techniques are imperfect, potentially opening new avenues for attack from outside actors. Security and ease of use don’t always go hand in hand, he said.

The wild west

Many early proponents of blockchain technology lauded its ability to operate outside of the usual restrictions and regulations of centralized governments and financial institutions. Although that lack of oversight is still welcome by many, a growing number of developers believe that some form of standardization and control is necessary to make blockchain a mainstream technology.

“I think [regulation is] certainly possible,” Monetha’s co-founder, Pikelis said. “There is so much uncertainty […] people still don’t agree on one kind of consensus on what they should do about cryptocurrencies and initial coin offerings (ICO). I think we’re going to see a lot happen in the regulation space for ICOs, cryptocurrencies and the blockchain quite differently in different parts of the world.”

Part of that will be financial regulation, he said, suggesting that bodies like the U.S. Securities and Exchange Commission will create guidelines for what is allowed. That will particularly affect companies looking to sell their own tokens.

Although regulating certain cryptocurrencies would be difficult, it’s not hard to look at the glut of new cryptocurrencies and blockchain marketing schemes and see the benefits of limitations. The expansion of blockchain into new areas also invites new regulations or running afoul of existing law. If it were used to track medical records, for example, it’d immediately become bound by existing laws in many countries across the globe.

“The whole attention to blockchain technology is a little bit premature, and the size of it brings a lot of pressure, and that’s why some things are starting to crack and some things might not seem rational,” Pikelis told us. “It will take some time for people who don’t have the tech savvyness and technical knowledge to be able to fully trust smart contracts and blockchain technology.”

It’s not hard to look at the glut of cryptocurrencies and blockchain marketing schemes and see the benefits of limitations.

We are starting to see the early signs of that, and as HashFlare told Digital Trends recently, the first steps will likely be know your customer (KYC) rules designed to prevent money laundering.

That’s unlikely to please those who have enjoyed operating on the fringes of society with anonymous cryptocurrency wallets and relative impunity from governing and regulatory bodies.

However, as with any new and exciting frontier technology, if blockchain wants to see more mainstream adoption, simplification of interaction and some form of remediation may be necessary – and that means governance.

That won’t solve everything though. Blockchain technology, by its very, distributed nature. That’s a strength in some cases, but also it hard to blockchain to handle some problems centralized systems have been designed from the ground up to achieve.

It seems likely that much, like the early days of the internet, some of the largest and most impactful blockchain platforms will one day become mainstays in everyday society. If that analogy if followed to its conclusion, though, it also means hoards of others will fall by the wayside to leave only the most useful and versatile standing. Blockchain is not a miracle cure for every technological ill and, as recent history has shown, powerful innovations come with unintended consequences.