The basis for Digit, a new service designed to help people save money automatically, really feels like it could also be the plot for a new Hollywood thriller. You connect your bank account to the service, it analyzes your spending, and then uses algorithms to slowly siphon un-noticeably small amounts of cash into a special savings account.

That description could easily apply to a rogue virus taking pennies here and there from unsuspecting people in order to fund any number of illegal activities. Luckily, Digit is using its power for good. At least I hope it is; I’ve been testing it for a month.

By far the most confusing thing with Digit is its lack of app, or consumer-facing interface.

I’ve never ever really run into a problem saving enough money to plan for the future, but, like everyone, I do wish I could save more. Because whether you’re a chronic spender or tight with the cash, it’s hard knowing how to keep a balance between saving and spending. Digit promises to strike the right balance without you lifting a finger.

I’ve tried Coin, the new credit card which puts all your card into one swipe-able card. I’ve also used Simple, the online-only bank account that promised a reinvented bank experience for a new generation. The problem with Coin, Simple, and the multitude of other new personal finance apps and services is that none has fully delivered on that reinvention promise. I’ve always been left feeling disappointed, even if there was some useful utility.

All of those new finance services have brilliant ideas that usually get held up in production or get watered down because of regulations. The idea for Digit is brilliant as well, but unlike the others, it has exceeded my expectations and really quickly changed how I think about banking.

The App-less App

First, here’s how Digit works.

On the company’s website, you sign up with your name and email, and then confirm a phone number — used for text messages. After the basic information, you link Digit to your bank account. With my bank account I was able to log in as I normally would online, and that was it. Basically, you’re giving Digit access to your account without actually giving it your credentials. Think of it as a “valet key” with special privileges, that you can also revoke at any time.

It’s that fast to getting a savings account setup with Digit. After which point you’ll probably spend some time figuring out how it works — considering there is no app that goes along with it.

Yes, by far the most confusing thing with Digit is its lack of app, or consumer-facing interface — especially because it’s dealing with important information like your bank account. In this regard you just have to trust it, a task I could imagine a lot of people aren’t willing to do.

Initially I spent a lot of brain power just trying to figure out the controls and what was going where, should I need to stop this crazy experiment. But once I understood that the money Digit was taking out was going into a completely separate (FDIC-insured) savings account, and how to use the few simple commands over SMS, I was more comfortable.

Less is more

It’s not easy getting over the lack of interface, but after a week with it, there’s definitely a new kind of freedom that isn’t present with regular apps. I’ll give you an example.

Opening a bank app and looking at the numbers can be overwhelming. It’s exciting if there’s a lot of money, but depressing if there’s not. While I can still see both my checking balance and my Digit savings balance, each with a quick text message, I’m not overwhelmed by the numbers. Using SMS, I’m getting the same information, but it doesn’t feel like traditional banking — the different context helps give perspective.

Using SMS, I’m getting the same information, but it doesn’t feel like traditional banking.

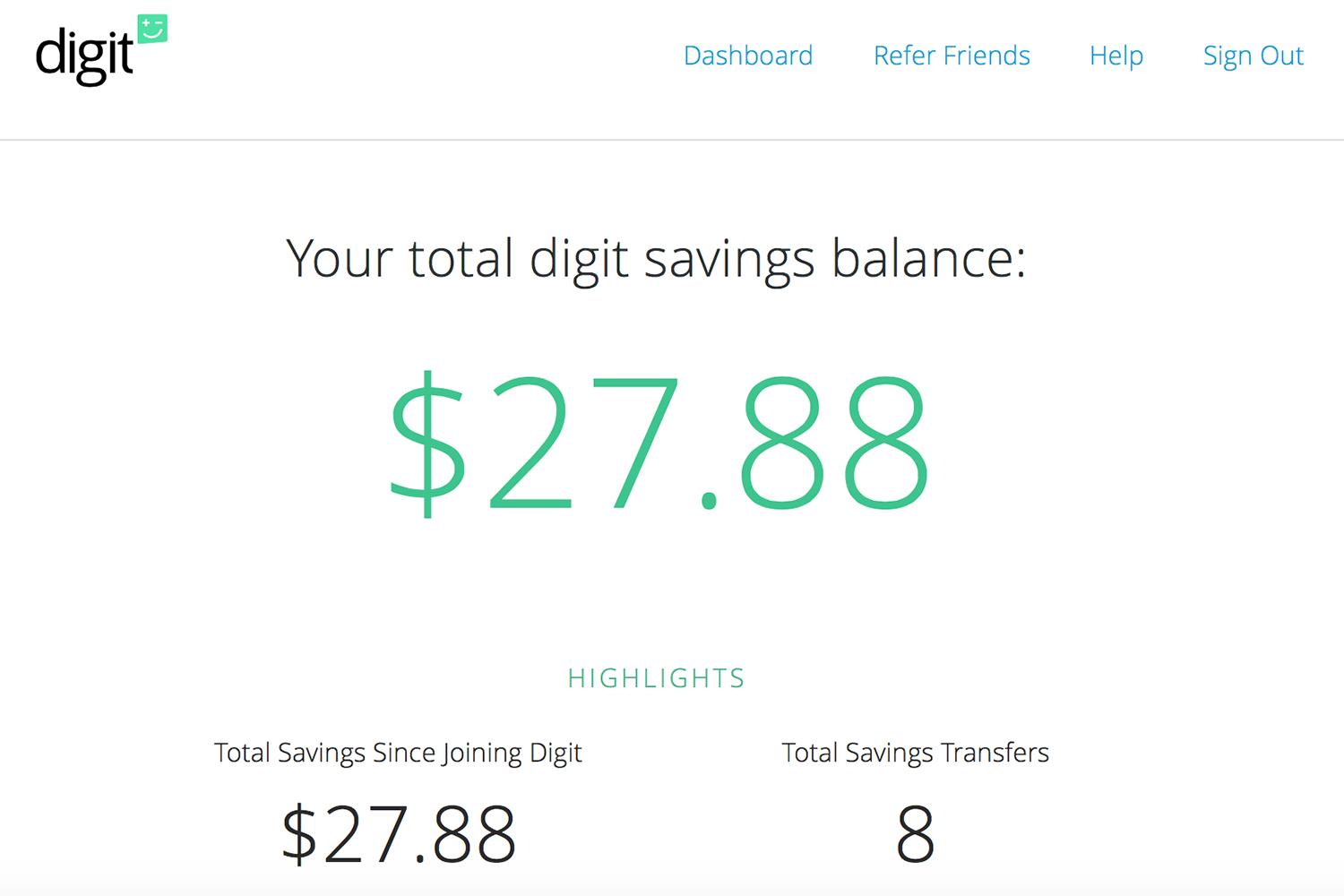

Not every app could go app-less, and I wouldn’t want a lot to, but Digit manages to pull it off. If you need a little more than some text bubbles, Digit does provide a visual dashboard on its site. It tells you your savings balance and a few stats, but all the interactions still happen over SMS.

The SMS interaction has been great in other ways too. I’ve fallen in love with the daily account balance texts it sends. In a world where everything is based around a recurring subscription fee, it’s incredibly handy to see what’s happening on a daily basis. It also doesn’t feel like you’re stress-checking your bank account multiple times a day.

At any time, I can type “balance,” and see what’s in the bank. I can also type “why,” and see the last three item descriptions.

It’s this simple functionality — both with saving extra bits of money and text balance inquiries — that should have come from banks directly. If a third-party like Digit can do it, there’s no reason the banks couldn’t.

That’s the only thing I worry about with Digit: Either it will be snatched up and acquired by a financial institution — maybe one I don’t use — or banks will start offering this functionality themselves.

In fact, Chase already has an automatic savings function where you can schedule money to automatically transfer to another. This is a fixed amount, however, compared to Digit’s algorithmic amount. That’s Digit’s secret sauce: It’s trying to save you money without you feeling the pain of saving money. One week it might make sense to only save $10, while another week saving $55 makes more sense.

It all adds up

I’ve spent almost exactly a month using Digit, or rather, letting Digit work while I did nothing, and it’s been great. Beyond the initial fear of signing up and connecting it to my bank, there hasn’t been any issues or concerns. I’ve let the service remain conservative, I haven’t told it to save more, and I’ve saved roughly $28 so far.

It’s not a crazy amount by any stretch, but having a couple hundred dollars extra around Christmas time is always helpful. Plus, if you do really want it to help you save, having Digit be more aggressive with your savings might actually net you a healthy sum after a while.

Are you wondering what the catch is with this free service? Your Digit savings account isn’t earning any interest. Digit is keeping the interest earned off the money being saved. If you’re putting away thousands and thousands of dollars, that might be an issue, but interest on consumer-level savings accounts haven’t been worth anything in decades, really. In terms of trade-offs so the company can continue operating without selling your data and showing ads, I think it’s a best-case scenario.

I’ve come to really like Digit. And while it might not actually be a crazy movie plot, Digit does actually live up to its promised potential. It can help you save money and gain control over your bank account.